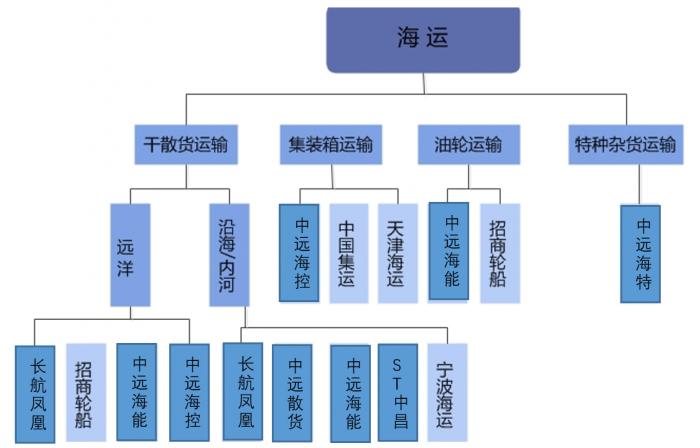

Figure Marine Transportation Major Listed Companies

The main maritime transportation in the country is concentrated in the hands of China COSCO SHIPPING Corporation Limited, with Changhang Phoenix, China Merchants Shipping, Ningbo Shipping, Tianjin Shipping and others occupying part of the shares.

Dry bulk: China COSCO occupies most of the Chinese market and specializes in ocean shipping, while China Shipping Group takes into account both ocean and coastal business. Oil transportation: China Shipping Development and China Merchants Shipping divide the market. Container: China Shipping Container Lines and China COSCO have a significant share, but compared with COSCO, China Shipping Container Lines is more specialized in its business.

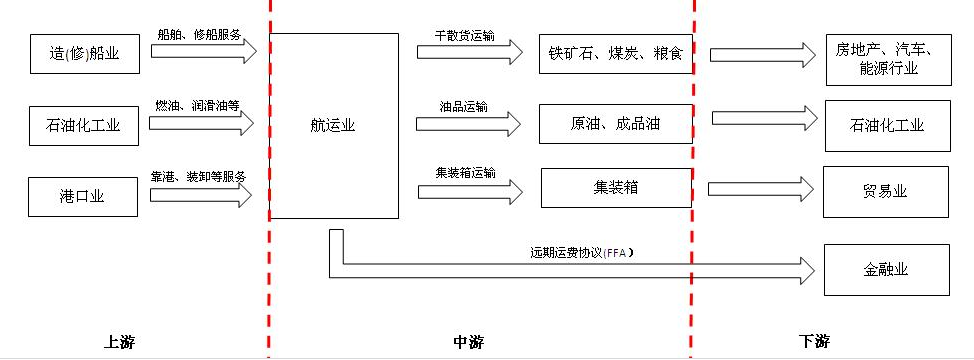

Figure Marine Transportation Industry Chain

Chapter 2: Business and Revenue Models

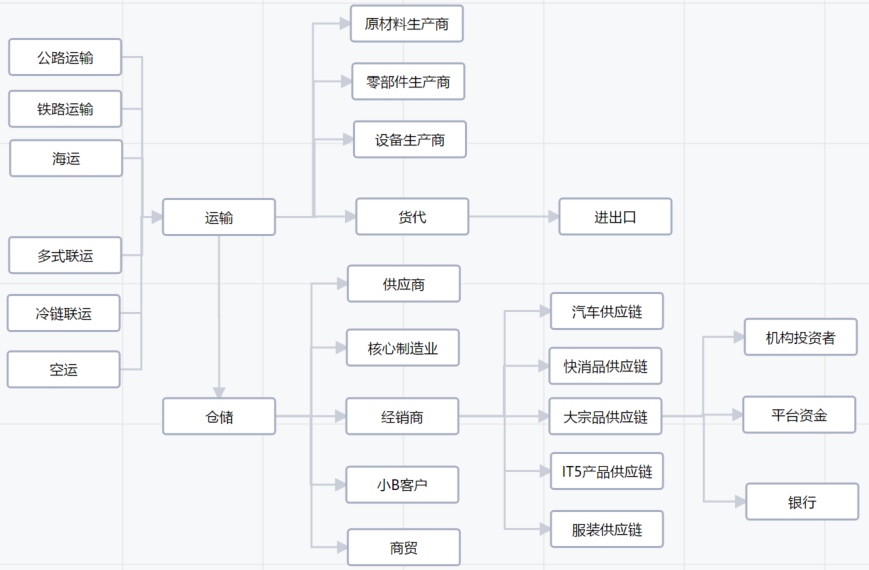

2.1 Marine transportation industry chain

Upstream of the maritime industry is the basic supply industry such as shipbuilding (repair), port terminals, etc., and downstream services such as steel, real estate and other basic industries of the national economy. The maritime transport industry is mainly divided into dry bulk transport, oil transport and container transport, etc. according to the different goods transported. The whole industry chain is transmitted from bottom to top, that is, the downstream transport demand will pull the boom and bust of maritime transport, and the longer cycle of upstream shipbuilding industry supply will increase the contradiction of industry supply-demand mismatch and cause more violent fluctuations in the cycle. In recent years, the maritime industry has become increasingly linked to the financial industry as companies increasingly use derivative instruments such as forward freight agreements (FFAs) to hedge their positions.

Figure Maritime Value Chain

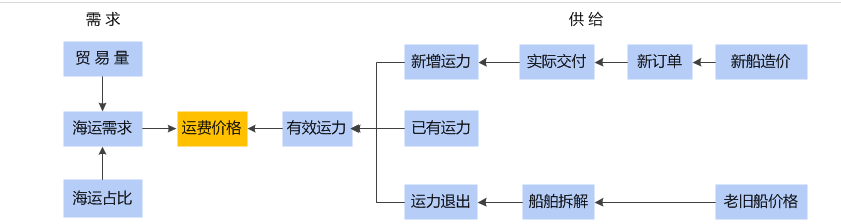

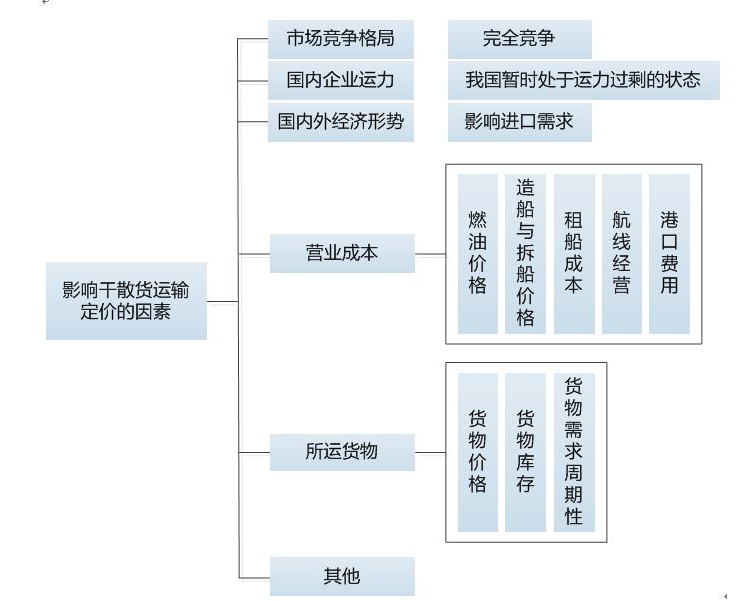

The analysis of the maritime industry is based on the analysis of supply and demand. The maritime industry as a global competitive industry, demand is mainly for global trade volume of dry bulk, oil products, containers, etc., and supply is mainly for the global ship capacity. The game of demand and supply is eventually transmitted to the price, which becomes the core factor affecting the change of profitability.

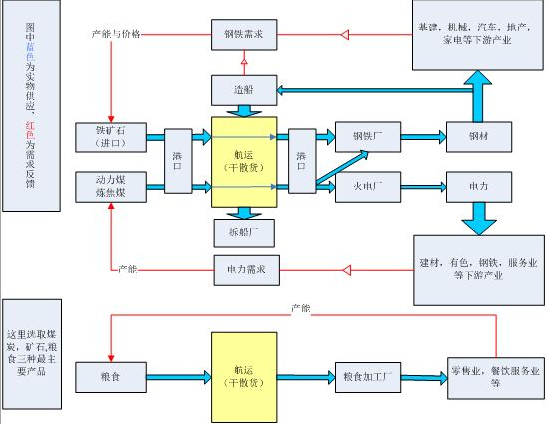

2.1.1 Dry bulk cargo transportation

The main cargoes of China's dry bulk shipping are three categories: various types of ores, coal and grain crops, and overall imports are much larger than exports. Ore and coal are intentionally put together here mainly because a large part of coking coal in coal will be used for smelting ore, and the two are highly correlated. Also note that the price of specialty steel affects shipbuilding, the upstream industry of shipping. Food and the other two have a low correlation, so they are listed separately.

The following pricing models are used for dry bulk shipping.

Table: Classification and basic information of dry bulk carriers

The main components of China's dry bulk shipping are iron ore and coal. Since China has completed the transformation from a major coal exporter to the largest net importer of coal in 10 years, the capacity occupied by China's dry bulk exports has been very little. China's iron ore compared with foreign ore grade is obviously inadequate, although the total amount of large but smelting costs are too high, it is better to import, so the country's iron ore is basically imported. China's iron ore and coal imports as a whole are very obvious upward trend, coal since 09 years more so. Since coking coal is mostly used in steel smelting, the import quantity of iron ore and coal has a great correlation, and ore and coal account for more than half of the global dry bulk seaborne trade. after 2003, China's strong demand for ore has made the Chinese factor gradually become the dominant global dry bulk trade.

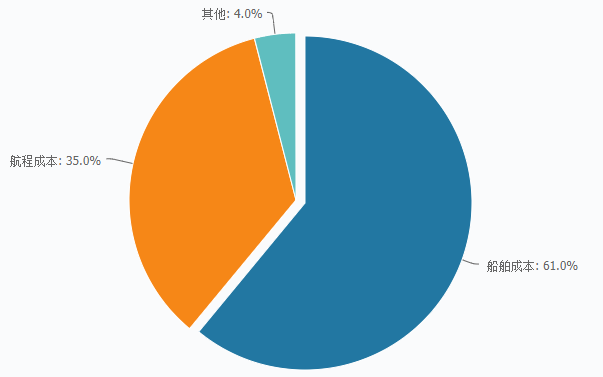

Figure: Cost components

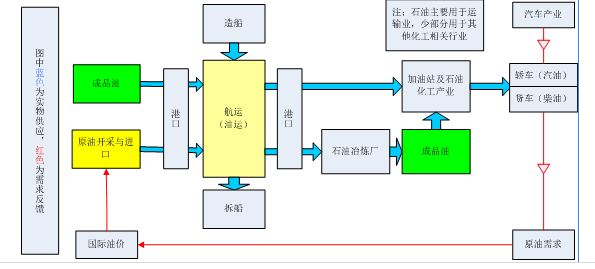

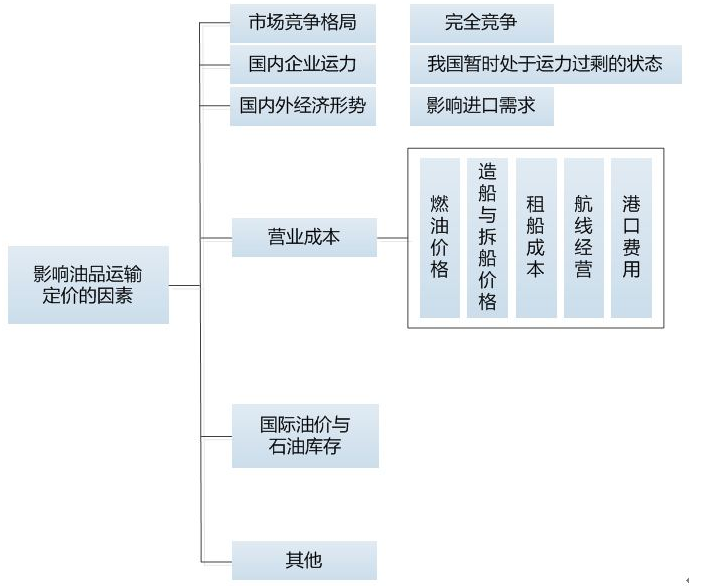

2.1.2 Oil transportation

The main cargoes of oil transportation are two types: crude oil and refined oil. Crude oil is not used directly, but goes to petrochemical companies for smelting. After smelting, the refined products will be shipped and transported by land to all parts of the country. Some of our refined oil products are imported directly, and most of them are smelted from imported crude oil.

The following pricing models are used for oil transportation.

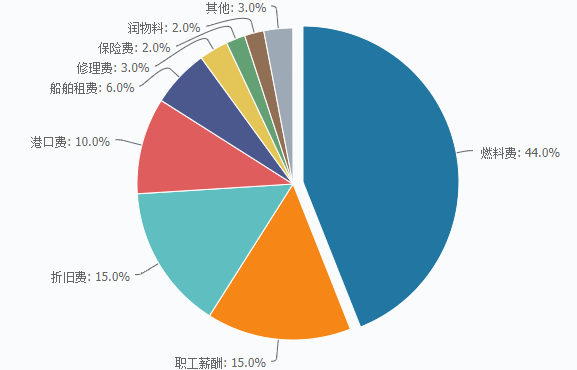

The costs of oil transportation are mainly focused on three areas: fuel costs, depreciation and employee compensation. Of these, fuel costs account for a relatively large portion and are affected by international oil prices, making them a relatively unstable factor in costs.

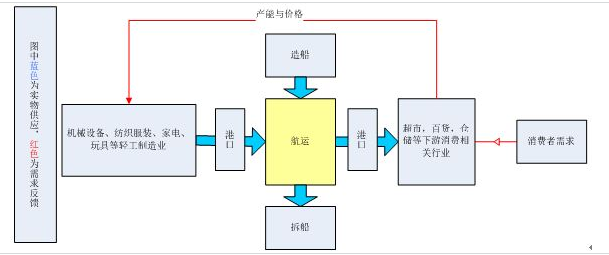

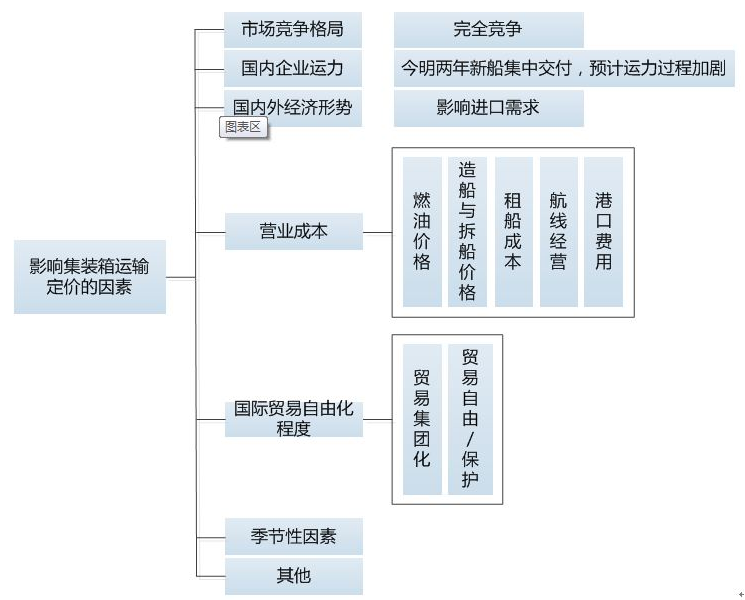

2.1.3 Container transportation

The chain structure of container shipping is relatively simple, but the materials involved are complex. The highest proportion of the transported goods are machinery and equipment, textile and garments, home appliances and toys. As the transported goods are basically finished products, the associated downstream industries are mostly sales industries. The container shipping business mainly comes from the export of light industry manufacturing. China's light industry export has obvious seasonality, especially the Spring Festival holiday in February every year directly lead to export volume cut off about one-third, while around December every year is the peak export season. Therefore, China's container shipping also has obvious seasonal changes. From the point of view of export amount, the proportion of each part is more stable so far in 2009. Electromechanical and high-tech products account for the bulk, followed by clothing.

Table: Container ship classification and basic information

Container shipping business mainly comes from the export of light manufacturing industry. China's light industry exports have more obvious seasonality, especially the Spring Festival holiday in February every year directly leads to the export volume cut off about one-third, while around December every year is the peak export season. Therefore, China's container shipping also has obvious seasonal changes. From the point of view of export amount, the proportion of each part is more stable so far in 2009. Electromechanical and high-tech products account for the bulk, followed by clothing.

The following pricing models are used for container shipping.

2.2 Typical company operating income and cost analysis

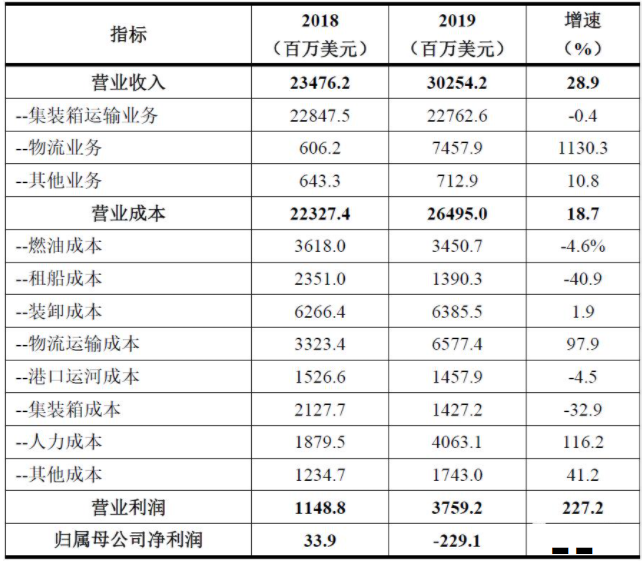

Table: Duffy Group Key Operating Indicators for 2019

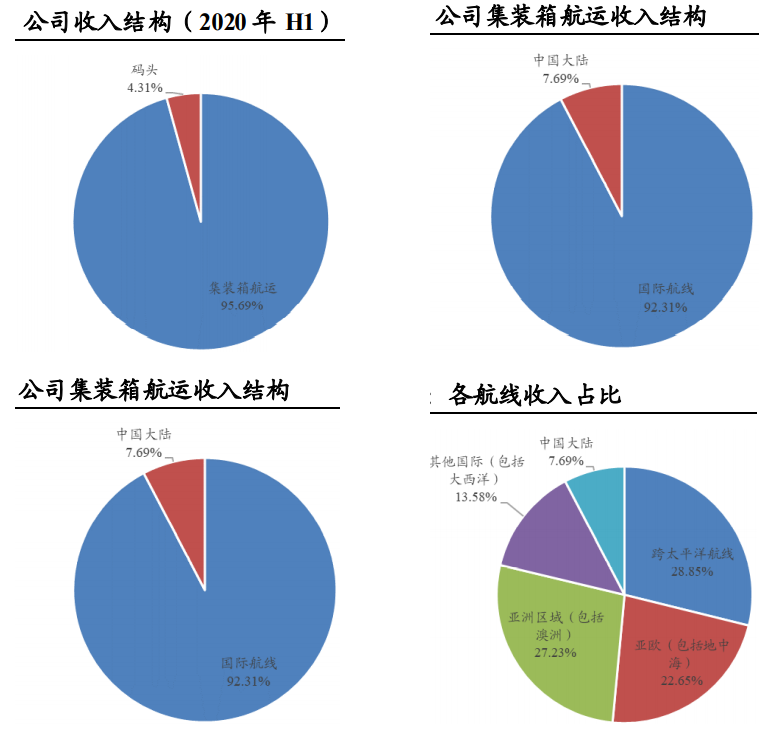

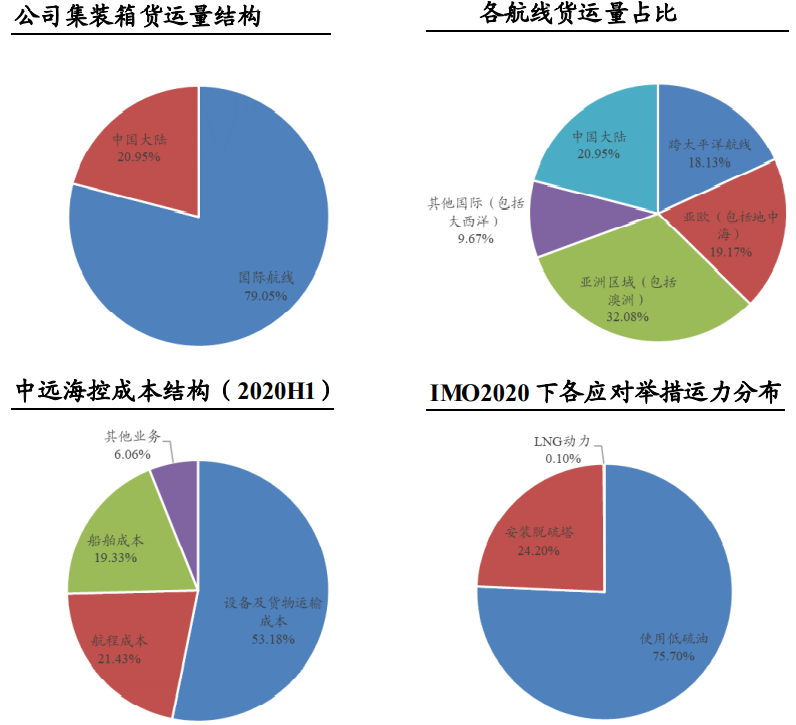

Fig. COSCO China Holdings' revenue cost and business breakdown

Chapter 3: Industry Valuation and Global Leaders

3.1 Comprehensive financial analysis of the industry

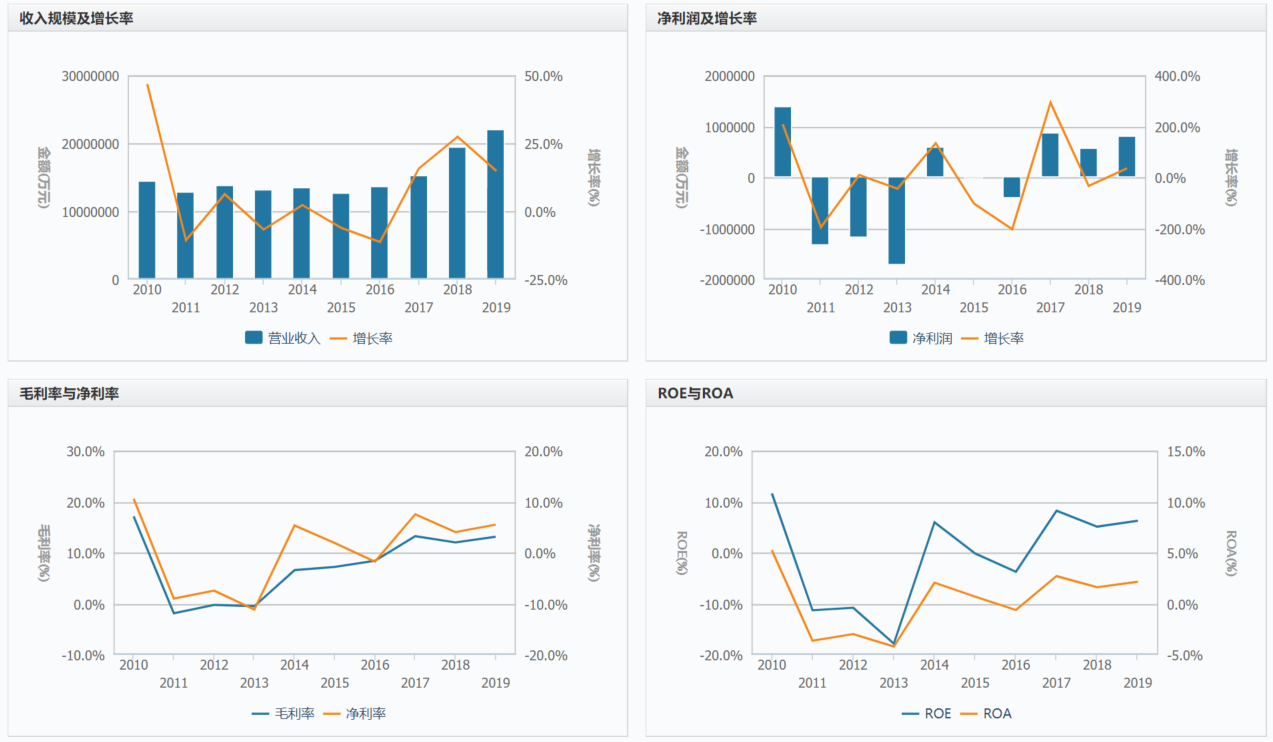

Figure Comprehensive financial analysis of the industry

Figure Industry Performance Analysis

3.2 Development and price-driven mechanisms

Maritime transport is an industry that is extremely dependent on import and export. The rise and fall of import and export determines the rise and fall of maritime transport. Among them, the world shipping center will be transferred to China under the impetus of the rapid development of economic and trade in Asian region, Asian shipping industry has been developed significantly, and international shipping resources are further concentrated to Asian region, and its center of gravity is being transferred to East Asia, especially to China. China is building three international shipping centers based on Bohai Bay, Yangtze River Delta and Pearl River Delta, namely the northern shipping center supported by Tianjin, Dalian, Qingdao and other ports, the Shanghai international shipping center with Jiangsu and Zhejiang as the two wings and Shanghai as the center, the Hong Kong international shipping center supported by Shenzhen, Guangzhou and Hong Kong, which is in line with the eastward shift of the world economic center and The requirements of China's rapid economic development.

In the history of world shipping for nearly 300 years, the boom and bust of the shipping market has almost always performed a trajectory of alternating cycles of change. The reasons for this cyclical round-trip cycle either accompany the boom and bust of the world economy or the process of war, scientific development and the development of human civilization. For centuries, this cycle of booms and crises in the shipping industry has occurred essentially once every 10 years, week after week. In the shipping market, both supply and demand are highly cyclical. A strong recovery on the demand side usually drives capacity on the supply side into a growth cycle after 2-3 years. Therefore, capacity supply has a certain lag. In turn, capacity growth will affect the balance of shipping supply and demand. Generally speaking, the capital expenditure cycle in the shipping market is the main determinant of the profitability cycle.

Along with the development of the world economy and the shift of the center of gravity, the international shipping center from Western Europe to North America, and then to East Asia progression. Western Europe, represented by Rotterdam, is an important international hub port in Europe; New York and Los Angeles represent an important international hub position in North America; when the center of gravity of world economic growth shifts from the Atlantic to the Pacific, Asia-Pacific ports, represented by Singapore and Hong Kong, rely on their superior status and position and have gained unprecedented development. According to the type of goods, sea transport is mainly divided into container transport, bulk cargo transport and tanker transport, which is transferred from goods producing countries to goods consuming countries through sea transport.

Figure: Transport chain derivation

The maritime industry is capital, technology is very intensive industry, but also high input, high-risk industry, its assets, technology characteristics determine the asset repositioning cycle is long, backward production capacity is slow to eliminate. In the case of backward production capacity flooding the market, the industry-wide downturn is difficult to change the situation. Reorganization and acquisition to become bigger and stronger is one of the channels to enhance competitiveness.

3.3 Domestic company ranking

3.4 Global Key Competitors

Figure Global Shipping Ranking

Founded in 1904 and headquartered in Copenhagen, Denmark, A.P. Moller-Maersk Group (A.P. Moller-Maersk) has offices in 135 countries and approximately 89,000 employees worldwide, providing first-class services to customers in container transport, logistics, terminal operations, oil and gas exploration and production, and other activities related to the shipping and retail industries. services.

Maersk Line is the world's largest container carrier with a global service network. 2020 August 10, Fortune released the world's top 500 list, Maersk Group ranked 320th in the world's top 500.

Mediterranean: MSC, known as Mediterranean Shipping Company S.A, was established in 1970 and is headquartered in Geneva, Switzerland. MSC is a global shipping and logistics company with a presence in 155 countries by 2020, promoting international trade between the world's major economies and emerging markets on all continents. Since its inception, MSC has evolved from a single-ship operation to a global enterprise with 560 vessels by 2020 and a modern fleet equipped with the latest green technology, which covers 500 ports on 200 shipping routes and carries approximately 21 million TEUs (in 20-foot containers) per year.

China COSCO SHIPPING Corporation Limited focuses on the four strategic dimensions of "scale growth, profitability, anti-cyclicality and global company", and focuses on the layout of shipping, logistics, finance, equipment manufacturing, shipping service, socialization and Internet+ related businesses. The company will further promote the integration of shipping elements and build a leading global integrated logistics and supply chain service provider by laying out the "6+1" industry clusters of shipping, logistics, finance, equipment manufacturing, shipping services, social industries and Internet+related business based on business model innovation. As of September 30, 2020, China COSCO Shipping Group operated a fleet of 109.33 million DWT/1,371 vessels, ranking first in the world. Among them, the container fleet is 3.16 million TEU/537 vessels, ranking the third in the world; the dry bulk fleet is 41.92 million DWT/440 vessels; the tanker fleet is 27.17 million DWT/214 vessels; and the miscellaneous special cargo fleet is 4.23 million DWT/145 vessels, ranking the first in the world. China COSCO Shipping Group's perfect global services have built up the advantages of network services and brand advantages. The upstream and downstream industrial chains, such as terminals, logistics, shipping finance, ship repair and shipbuilding, have formed a more complete industrial structure system. The Group has invested in 59 terminals worldwide, 51 container terminals, and the annual throughput capacity of container terminals is 126.75 million TEU, ranking first in the world. Global ship fuel sales exceeded 27.7 million tons, ranking first in the world. The scale of container leasing business holdings reached 3.7 million TEU, ranking second in the world. The scale of orders received for marine engineering equipment manufacturing and ship agency business also steadily ranks among the top in the world.

Chapter 4 Future Industry Outlook

The shipping industry has always been regarded as an important pillar industry of a country, and governments attach great importance to the nationalization attributes of shipping enterprises. Cargo volume growth is slowing down, and the situation of overcapacity has not been fundamentally improved while cargo volume growth is being tested.

Market concentration is increasing, with mergers and acquisitions and alliances continuing and dominating market share. Changes in the internal and external environment have also made the liner industry change, while some new trends emerged. In recent years, the pace of consolidation in the global container shipping industry has accelerated, with mergers and acquisitions of liner companies and several reorganizations of shipping alliances. At present, three alliances dominate the container shipping market and occupy the majority share on the three major trunk routes in the east and west.

In 2030, China will continue to stabilize its position as the world's largest cargo trading country and will dominate the global container shipping trade. 2030, China's total international shipping volume is expected to be 6.2 billion tons, accounting for about 17% of the global shipping volume; among them, the growth of iron ore and coal demand in dry bulk transportation will slow down significantly, grain and oil imports will grow faster, and international container The total volume of import and export sea cargo will exceed 200 million TEU.

(作者:千际投行 )

声明:本文由21财经客户端“南财号”平台入驻机构(自媒体)发布,不代表21财经客户端的观点和立场。